Downward nominal rigidity also explains why unemployment is correlated with wage inflation not the acceleration of wage inflation (that is the change in wage inflation) or wage inflation minus expected price inflation. 21st century data look like the original Phillips scatter and like the expectations unaugmented Phillips curve (which was never actually taken seriously by more than one or two macro-economists in the 60s). As argued by Akerlof Dickens and Perry in 1996 (and informally by many others back in the even older days) if there are different markets for labor (different places, different industries, different occupations requiring different skills) then the relevant unemployment rate will be different for the different labor markets. With high unemployment and low expected inflation, many wage changes will be zero & stuck at the lower bound. higher constant not accelerating inflation relaxes this lower bound (which is that nominal wage changes can't be negative). This causes higher employment (and lower real wages). This gives a stable downward sloping Phillips curve (at least sloping down at very low inflation rates). The argument is important, because inflation also makes it easier for relative wages to adjust which (in the model) causes higher productive efficiency and average welfare.

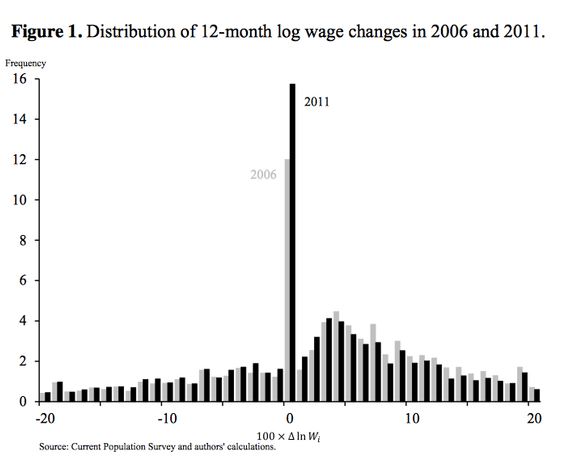

I think the puzzle of why average wages continued to grow at a rate well above zero isn't completely solved. I can't imagine that in 2009 and 2010 there were many particular labor markets with enough demand to cause high wage increases (I'm sure the tails in the Daly and Hobijn figure are due to people losing good jobs and moving to bad ones or finding better jobs).

I think that the standard scheduled increase in wages with increased seniority might be binding too. If there is a contract (or an explicit contract) which says that wages increase 1% for every year of seniority, it could be infuriating for the firm to pay only last years nominal wage.

It is also true that with the high unemployment rate, the quit rate declined dramatically in 2009 and stayed low. This would make the promise of an increase of wages with seniority binding. Another way of putting it is downward nominal wage rigidity (with or without seniority based pay increases) means workers have wages higher than other employers want to pay (but are still worth employing for their current employer because of firm specific training). This means their wage is higher than the market wage. Higher and rising with seniority as promised.

I think this could explain the mass of wage increases around 3% to 4%. It isn't a spike like the spike at 0%, because different contracts have different provisions (and implicit contracts are vague). Or it could just be the normal normal.

6 comments:

"I think the puzzle of why average wages continued to grow at a rate well above zero isn't completely solved."

Hiring and training costs are an important factor. Most job training is "on the job". Many employers have idiosyncrasies that must be learned. If a trained employee leaves, the cost of replacing the employee may be much more than the wage increase needed for retention. A higher paid employee may have to not do some higher level work to cover for the lost worker. Institutional memory makes employees more valuable as they age. Companies do compete for workers. Workers can advance by moving up in a company or by moving to another company. This competition will always cause wages to increase.

https://research.stlouisfed.org/fred2/graph/?g=2oVc

January 30, 2015

Employment Cost Indexes for compensation and wages & salaries and Unemployment Rate, 2002-2015

(Percent change and Percent)

-- Anne

I like this essay quite a bit.

-- Anne

Also, do add paragraphs to make for easier reading.

Do comments work? No sign they post.

Really nicely done.

Anne

Post a Comment